Too bad for the tax payer

Socialising the losses and privatising the gains – Part 2

On 4 May 2018, in anticipation of what seemed to be cooking at the Co-op, I wrote an article with the title of “Socialising the losses and privatising the gains”[1] where I warned of what was likely to take place and also in order to make people aware that the most likely outcome would be the camouflaging and the passing on to the tax payer of the huge losses that seemed inevitable. I also anticipated that an attempt would be made to make the investment proposition attractive for potential new investors by creating and putting on the table some government backed risk free assets. However, I never imagined the extent of the damage that five years of state ownership and mismanagement could have caused. Nor did I anticipate how bad from the point of view of the tax payer any package to be presented to a new private investor would have to become in order to make the deal happen.

I have constructed Table 1 from reports in the media and by reading a little between the lines so as to reveal the facts from what dubious statements the Government itself was making in order to camouflage the bitter truth. Although I am pretty sure the numbers are correct, I cannot at this juncture verify what has been reported. When and if ever we have a full and detailed account of what has taken place and agreed I may need to revise the table. Be that as it may, the conclusions that one derives from the comprehensive picture the table presents are hard to escape from:

- This deal is too good to be true from the point of view of the major shareholders of Hellenic Bank and a total disaster from the perspective of the tax payer.

- The extent of the damage that the state owned and incompetently managed Co-op has inflicted on us during the past five years is beyond belief. If one excludes the support money Cyprus received for the recapitalisation of the Co-op itself (€1.7 billion) the total cost to the taxpayer from the present self-made calamity is larger than the money received and used under the European Adjustment Program[2] in 2013.

- It has now become almost abundantly clear that the Government and the management of the Co-op have been covering this up. As recently as a few months ago, they were submitting reports to the Cyprus Stock Exchange for approval that showed the Co-op as profitable and with a sound balance sheet. They even passed through a Ministerial Council a decision for giving away shares to “some customers” of the bank.

- There was an obvious and conscious attempt with various pretexts (regarding social responsibility and in order “not to cause a bank run”) to keep this under wraps so that they could get President Anastassiades re-elected.

- Last but not least, they now have the audacity to present themselves as heroes and the people’s saviours. And they do this in a sinister manner by carefully and systematically constructing false statements. For example, they often refer to the Government bonds they issue to entice Hellenic Bank to accept the deal as deposits rather than calling it what it really is - giveaways.

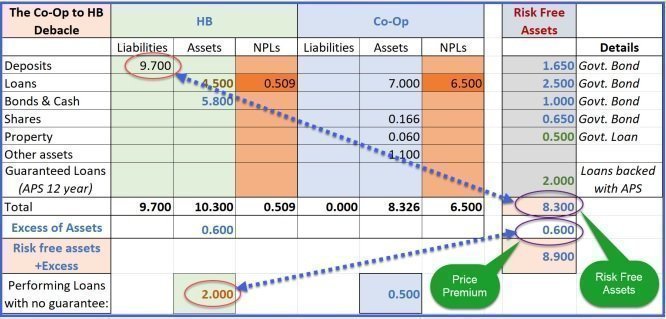

In compiling Table 1 below, I tried to apply my expertise in assessing project finance projects, where one has to identify and evaluate the risks and then determine how best to reduce and allocate these among the participants in such a deal. In my 30 years experience with such projects, I have never come across such a one sided deal. As the column headed “Risk Free Assets” shows, the Government puts up risk free “goodies” of the order o €8.3 billion. In addition, the assets received by the other party exceed the liabilities they undertake by €600 million. The two total to about €8.9 billion. The only chunk of assets Hellenic Bank is taking any risk on is the €2 billion of non-guaranteed but performing loans it has selected and which potentially can turn into non-performing. However, these loans are not only performing, but they are also very well secured by collaterals and guarantees. Given that HB is gets a price premium for the risk assets it receives on this deal, in order to lose any money by having these loans going bad, as the table demonstrates, it has to fail in its collection/recovery efforts (in net present value terms) to below €1.4 billion out of a total of €2 billion of performing and well secured loans.

Table 1- The deal through the risk perspective

So, in conclusion, let’s call this what it really is. The Co-op is probably facing bankruptcy and is surely in grave need for recapitalisation that is however no longer possible from government funds. This in itself raises a host of questions, such as why is the liquidation process not applied or the new EU law that prescribes how to deal with such situations for systemic banks come into effect? What are the SSM or the Central Bank’s roles and responsibilities in this? Why do these institutions stand by and watch while they allow the Cypriot tax payer to pick up the bill? Are these enormous Government giveaways not State support and in violation of EU competition laws? When and how will the individuals who brought about this disaster upon the people of Cyprus be held accountable? Last but not least, why is every one sitting back and allowing this deal to go through and only then perhaps dare ask any questions?

Savvakis C. Savvides is an economist, specialising in economic development and project financing. He is a former senior manager at the Cyprus Development Bank and has been a regular visiting lecturer at Harvard University and currently at Queen’s University. Author page: http://ssrn.com/author=262460.

[1] Savvides S., Stockwatch, https://www.stockwatch.com.cy/el/blog/640941-socialising-losses-and-privatising-gains, 4 May 2018

[2] Only about €7.2 billion have been used out of a total of €10 billion approved by the ESM for Cyprus.