An Alternative Way to Deal with the Cyprus Co-Op Bank

Socialising the losses and privatising the gains

I have written two articles on the subject of “the Deal” sought and negotiated by the Government for privatising the ailing Co-Op Bank in Cyprus. I continue here with “Socialising the losses and privatising the gains - Part 3” which provides an alternative proposal than the one that the Government arrived at with Hellenic Bank. It makes the argument that the concessions made in desperation to the Hellenic Bank (which was the only bidder) can be employed with less risk for the people and more usefully for the economy to create a new financing institution which would undertake the much needed task of reconstructing and developing the economy on a sound and solid footing. The deal reached with the Hellenic Bank and put forward for Parliamentary approval is fraught with many risks and comes at very high costs for the Cypriot tax payer. There is another, a better way to diffuse the Co-Op conundrum and turn it into a positive instrument for sustainable development. This article is in sequence to my previous article “Too bad for the tax payer: Socialising the losses and privatising the gains”[1] which should be read first as it puts this one into context.

The ugly side of the Co-Op deal

The gist of this deal is that the Minister put on the table (using tax payer money) whatever it took to persuade the shareholders of HB to take the deposits off them. A question being raised is whether indeed the Minister could do this without prior Parliamentary approval and the vetting of the agreement by the Attorney General. But there are far more serious and pertinent issues the tax payer should be concerned about this deal.

The underlying rationale for this is one sided agreement is that the risk of paying the deposits is passed on the buyer. This unfortunately is a complete myth, or at the very least, a misconception. Since these deposits are almost all under €100,000 the risk of paying them off remains with the Government (under the Depositors’ Guarantee Scheme) whether they transferred to a private bank or not.

HB had every right to ask for the moon and the sky in order to cover the gap between the liabilities (the deposits) and the very selective assets they cherry picked. The Minister however should then have considered his options. They asked for the moon and the stars because they knew that the Minister would probably bring the Government down if he admitted that the "privatisation" failed and that the Co-Op was going into liquidation and possibly a bail-in.

So, the Minister, with nowhere to go apparently, opted to create giveaways and disguise it as if he was buying assets which were already owned by the Co-Op Bank. And he almost got away with it. What he was really doing was caving in to the outrageous demands of the only potential buyer and packaging Government bonds and other goodies (risk free loans - APS backed) and which made the asset side of the deal practically risk free for the buyer. Then he served this to the people as money spent to buy what already belonged to us! Not even Houdini could have managed this so well!

It is a delusion that the risk of paying the Co-Op is passed on. It remains with the Government. First and foremost those who know and understand this one sided risk exposure would be the new major shareholders of the Hellenic Bank who have in all probability taken this into consideration when deciding to participate in the required increase of the bank’s capital. It should be expected therefore that they will take full advantage of this frailty in the agreement when in control of HB.

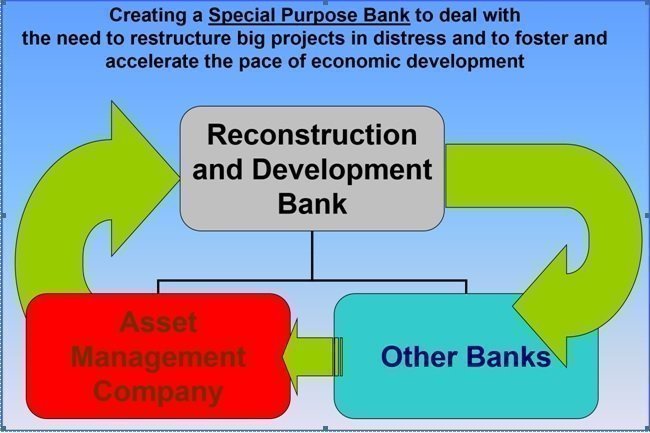

The Alternative way

Given the concessions made and the gifts that have been put together to hand over to the Hellenic Bank in order to entice them to take over the liability of the deposits (a risk which as argued above actually remains with the Government) one cannot help but wonder why the Co-Op Bank close down with two new entities created from its Assets and Liabilities which are in the current deal with HB. One would be the Asset Management Company (“Estia”) which includes in essence all the non-performing loans and the other assets which as per the agreement with the Hellenic Bank will be on its Balance Sheet. What remains and is being packaged to be handed to Hellenic is in essence an almost perfectly well capitalised and balanced in terms of risk bank. This new bank has to be given a mission and role that is proactively likely to help the ailing Cyprus Economy to recover. It should be manned by expert and competent professional personnel ready to take up the role of a much needed Reconstruction and Development Bank.

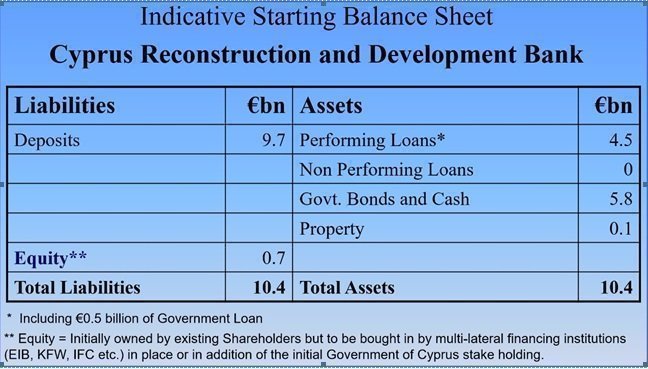

This new bank will have a robust balance sheet and at least to begin with it will be the healthiest bank with practically no non-performing loans and a built-in ability to restructure and spin back into the real economy viable and very bankable projects and businesses. An indicative starting balance sheet which in essence is no different than the one currently being packaged and intended to be handed to the Hellenic Bank is shown below:There two points that need to be made to clarify this proposal:

1. The Existing Co-Op will have to cease to exist (as the goodies thrown in by the Minister will be considered State aid and this is not allowed). But a new shell company can be created (a new entity) and that can take over both the assets and liabilities that are now heading to Hellenic where the new “investors” are anxiously waiting to suck the blood out of the assets in the near future (and of course let the deposits to be recovered from the Deposit Guarantee Scheme).

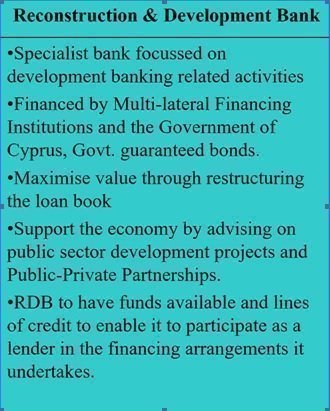

2. The bank that is to be created (which will have the healthiest balance sheet), will need to have a useful purpose to exist (a mission) and competent personnel to make this happen. This is why I keep proposing and shouting on deaf ears for five years now for the need to have a Reconstruction and Development Bank. I have written a lot about the need for this type of financial institution and what should be its main activities. The Government should in any case have majority control in such an institution, although like the CDB in the good years after the invasion, it should be totally independent, by law enactment if necessary, from political influence.

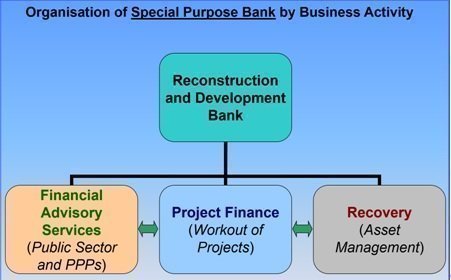

The structure and main activities of the new Cyprus Reconstruction and Development Bank is envisaged to be as shown below:

In more detail the Project finance activity will specialise on the need to work out viable business entities which are adequately capitalised and with a manageable level of debt to carry. The emphasis on corporate and business structuring and financing is crucial for both industry but also household loans. As the household’s capability to repay their own debt depends on their ability to be employed and having an income. It will also provide much needed expert assessment and be involved in the structuring of public sector and Public-Private Partnership (PPP) deals so as to ensure that only economically viable projects are undertaken and that the PPP agreements arrived at are to the benefit of the public at large. It will also have as by necessity and Asset Management arm to deal with the management and disposal of break down assets.

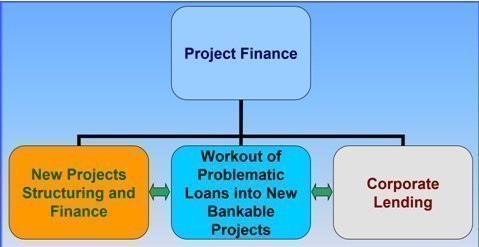

In more detail the Project Finance arm of the RDB can be as follows:

It is also envisaged at least initially that the new structure will operate the 72 branches as it is planned to be transferred to HB under the preliminary deal reached with the staff as needed to operate these branches (estimated to be about 1,000). But the basic human resource structure of the Professional part of the RDB can initially be no more than 150 employees but may increase to be up to 250, if needed.

The benefits of the above set up as compared to the deal reached with the Hellenic Bank are:

- No risk of running down the assets and ripping the balance sheet by vulture private investors.

- A system of competent professionals will be in place to aid the reconstruction of viable and credit worthy projects and businesses.

- RDB can lead by example, where other banks can find the competence they need and now lack for attaining viable restructurings into new special purpose vehicles structured after careful assessment of opportunities and risks by an expert organisation of economic development.

- If we miss the chance to take this opportunity to plan for the future we will surely be crying and be worse off in five years or even earlier this time.

In conclusion, the above proposal serves a real need for having a competent financing and restructuring institution which can fill the gap arising from the need to create from the underwater parts of a failed system and spin back into the real economy viable and bankable projects (both in the private and public sector) and businesses.

In summary, the main features of the RDB will be:

It is not too late to make the right decisions that will determine the economic future and welfare for us and our children. This is the time to have the courage to make the right decisions and act proactively rather than reactively, as we did in 2013.

Bibliography

- Savvides, Savvakis C., Corporate Lending and the Assessment of Credit Risk (March 1, 2011). Journal of Money, Investment and Banking, No. 20, 2011. Available at SSRN: https://ssrn.com/abstract=1813013

- Savvides, Savvakis C., Financial Markets, Bloated Governments and the Misallocation of Capital (May 31, 2012). Journal of Finance and Investment Analysis, Vol. 1, No. 2, pp. 201-219, 2012. Available at SSRN: https://ssrn.com/abstract=2070264

- Savvides, Savvakis C., Overcoming Private Debt (Unblocking the Loan Burdened Real Economy in Cyprus) (June 20, 2016). The Journal of Private Equity, Fall 2016, Vol. 19, No. 4: pp. 51-59. Available at SSRN: https://ssrn.com/abstract=2784680 or http://dx.doi.org/10.2139/ssrn.2784680

- Manison, Leslie and Savvides, Savvakis C., Neglect Private Debt at the Economy's Peril (December 1, 2016). World Economics Journal, Vol. 18, No. 1, January–March 2017. Available at SSRN: https://ssrn.com/abstract=2886345 or http://dx.doi.org/10.2139/ssrn.2886345

- Savvides, Savvakis C., Socialising the Losses and Privatising the Gains (The Case of Cyprus Five Years After the Bail-in of Bank Deposits) (April 30, 2018). Accountancy Cyprus, Vol. 130, May 2018. Available at SSRN: https://ssrn.com/abstract=3171049

- Savvides, Savvakis C., The Pursuit of Economic Development (April 8, 2014). Journal of Finance and Investment Analysis, Vol. 3, No. 2, 2014. Available at SSRN: https://ssrn.com/abstract=2441299

Savvakis C. Savvides is an economist, specialising in economic development and project financing. He is a former senior manager at the Cyprus Development Bank and has been a regular visiting lecturer at Harvard University and currently at Queen’s University. Author page: http://ssrn.com/author=262460.

[1] Savvides S., Stockwatch, https://www.stockwatch.com.cy/el/blog/640941-socialising-losses-and-privatising-gains, 4 May 2018.